Originally published September 7, 2022 in the CFA Institute’s “Enterprising Investor”

The number of environmental, social, and governance (ESG) benchmarks and indexes demanded by the asset management community has grown at an unprecedented rate over the past two years. That’s according to our latest survey of Index Industry Association (IIA) members. Unpacking these high-level numbers, ESG indexes have expanded beyond more traditional areas of integration into new asset classes and strategies.

The IIA queries our membership each fall in our annual benchmark survey to understand where the index industry’s growth is coming from. Last fall, the IIA found the number of ESG indexes increased 85% over the last two years. In response, we conducted additional surveys of the global asset manager community in 2021 and 2022 to confirm that index providers are meeting the ESG needs of the investment community, assessing the impact, and monitoring potential impediments to growth.

That’s what makes the results of our most recent ESG Global Asset Manager Survey so interesting. Conducted earlier this year, the survey queried 300 investment fund companies across Europe and the United States. It found that amid geopolitical conflict, rising interest rates in many countries, a 40-year high in inflation, and now recession fears, the influence of sustainable investment factors on the global market ecosystem has continued to accelerate.

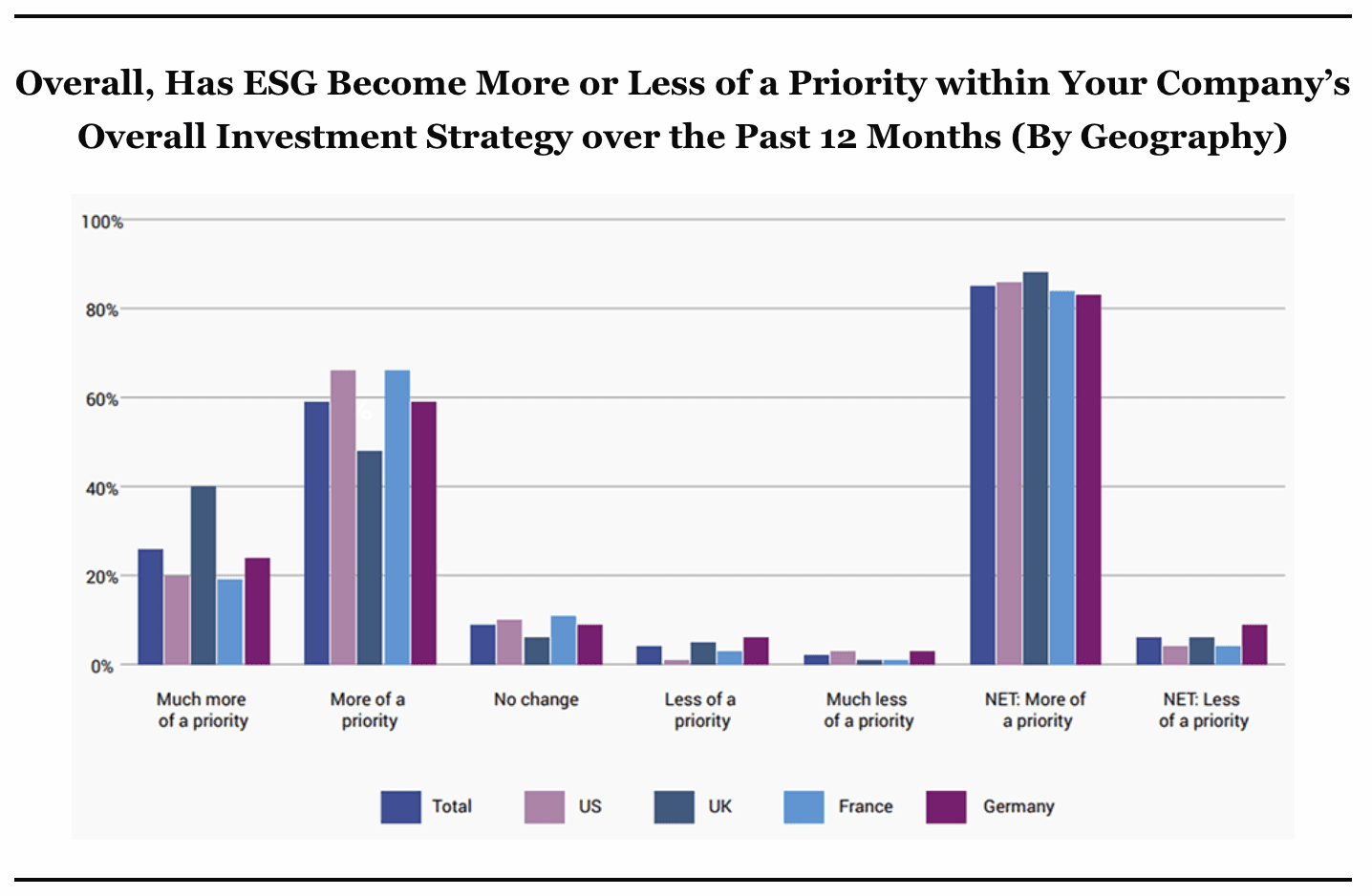

In fact, our survey found that ESG factors are even more important to global asset managers today than they were a year ago. A full 85% of asset managers reported that ESG has become a larger priority within their company’s overall investment strategy in the past year.

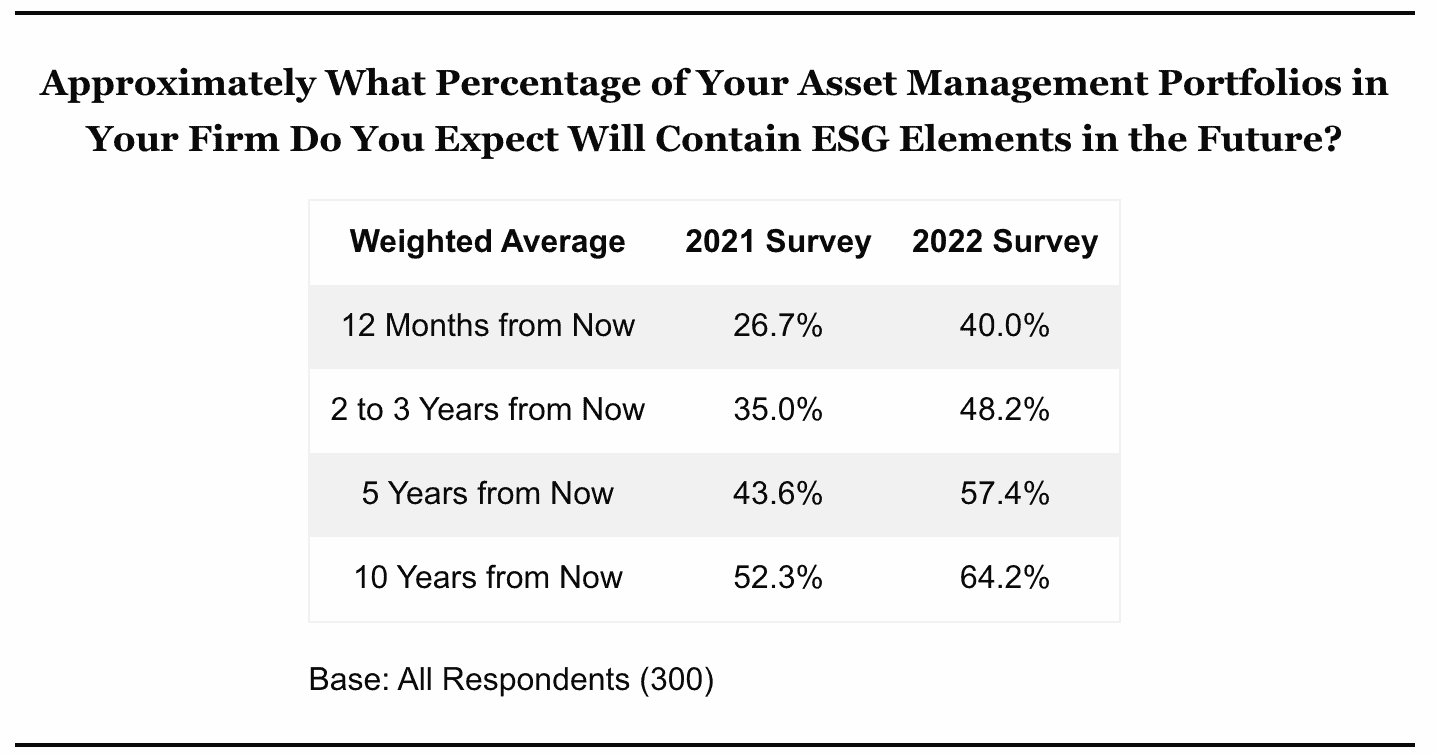

To be sure, given extensive media coverage of ESG and its aggressive promotion by asset managers, these results may not be all that surprising. So, we dug deeper on our next question and asked asset managers to quantify the integration of ESG considerations into their portfolios. We wanted to understand what asset managers believe the future state of asset management will look like. Expectations around ESG portfolio percentages within the next 12 months jumped more than 13% over last year’s survey. Moreover, within 10 years, asset managers expect 64.2% of their portfolios will contain ESG elements. These double-digit percentage increases over last year’s results extend across every time horizon surveyed.

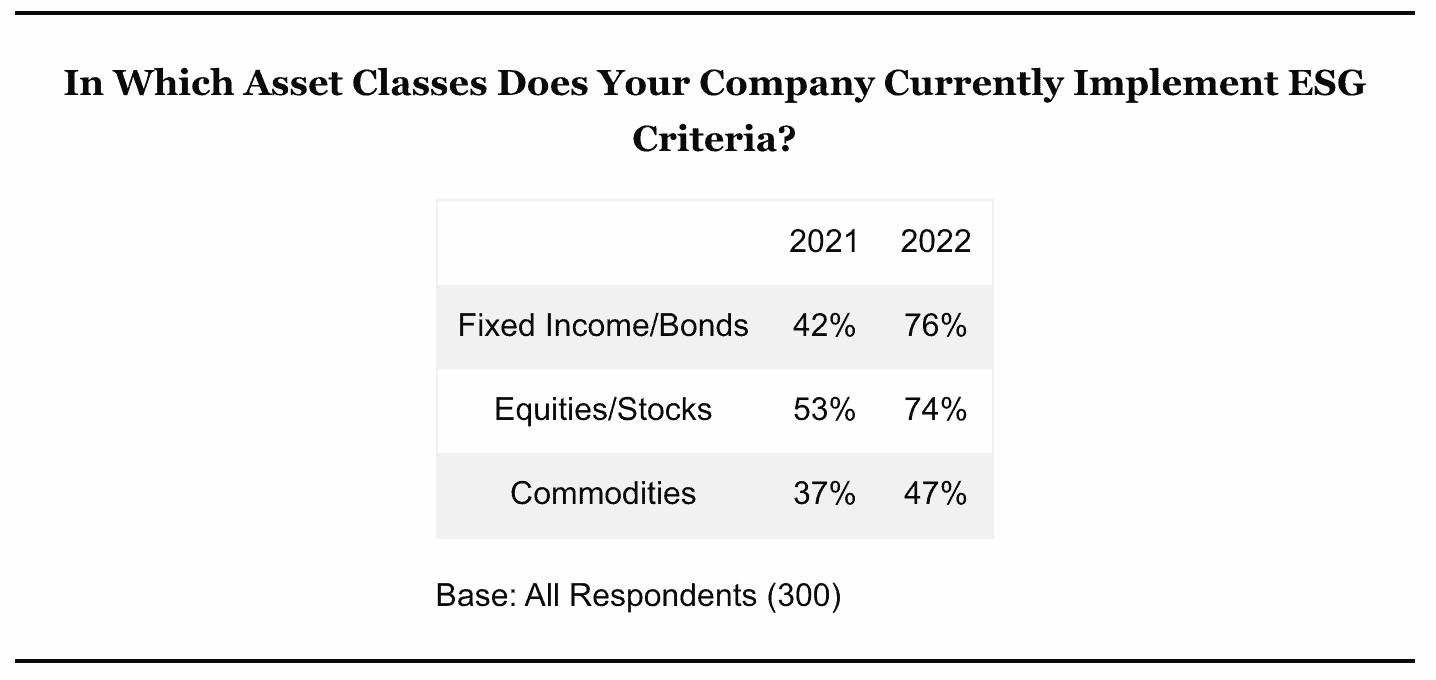

ESG integration has become so widespread that sustainable investment approaches have expanded beyond equities into other asset classes. The percentage of investors implementing ESG factors in their allocations to fixed income shot up to 76% this year, from 42% just a year ago. In fact, ESG integration in all asset classes grew year-over-year, with the most expansion in fixed income. This trend shows no signs of slowing: Over 80% of global asset managers expect the use of ESG criteria in all major asset classes to increase in the next 12 months.

What explains these results? Based on conversations with market participants, I believe better data has led to better ratings and more research and development in fixed income, which in turn has created greater impetus to incorporate sustainable investing across asset classes and portfolio holdings.

That conclusion isn’t purely anecdotal: More than 9 out of 10 survey respondents agreed that environmental impact, social sustainability, and corporate governance tracking tools, metrics, and services were either highly or fairly effective. That’s up significantly from 66% in 2021.

Of course, given concerns about greenwashing and disparate data across the E, S, and G, this result seems optimistic. To date, environmental data is more quantifiable and directly measurable than social and governance data. Within “E” ratings, agencies can standardize how emissions are measured across various jurisdictions, for example. By contrast, privacy issues make some social data difficult if not impossible to collect. More fundamentally, not every country or culture, let alone individual, agrees on what the specific social priorities ought to be.

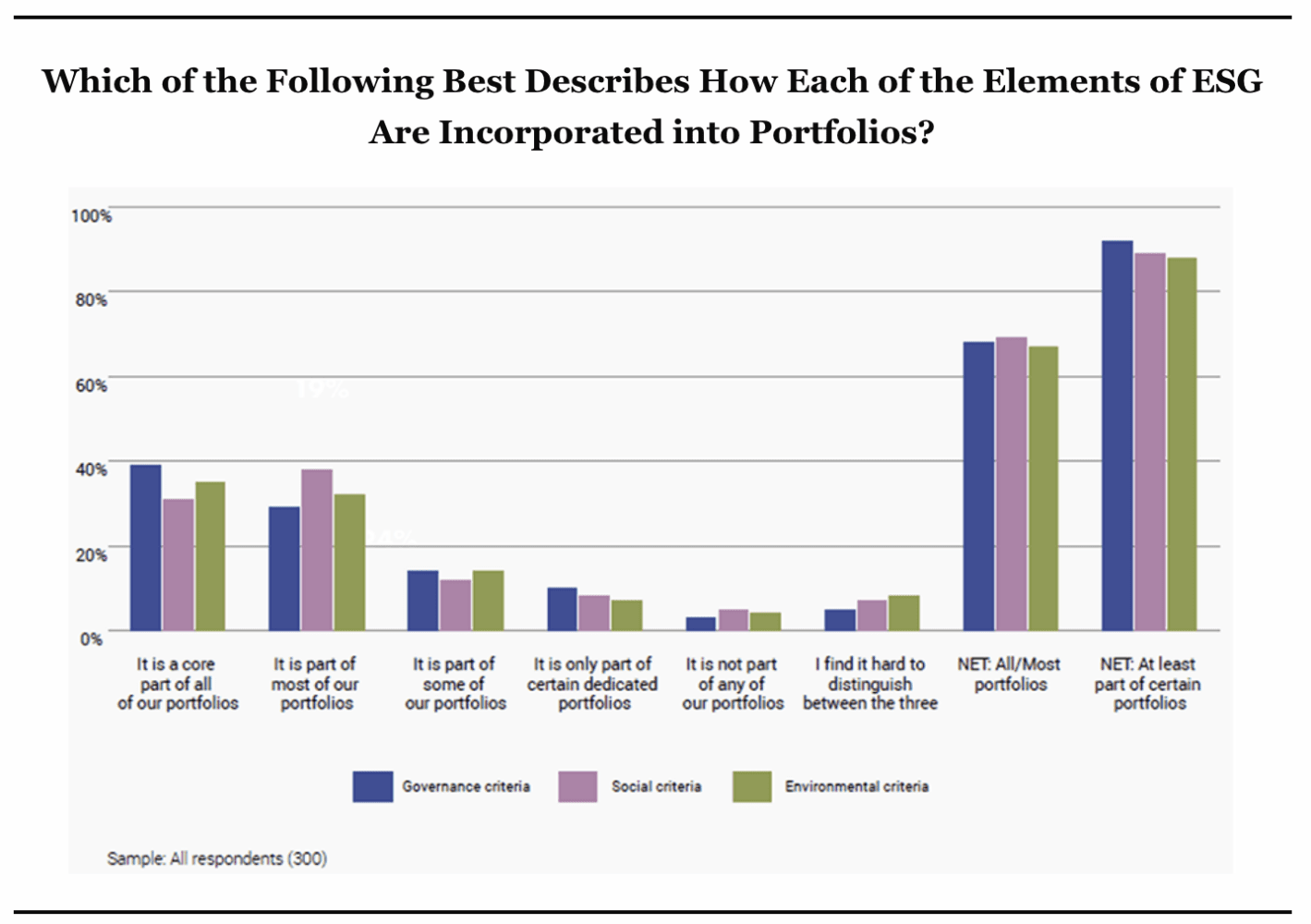

But the survey responses do indicate something of a paradox: Fund managers are giving broadly equal weight to the E, S, and G components even as their attitudinal comments suggest that environmental concerns are more top of mind at this stage of ESG development. In fact, 78% of respondents said that “environmental criteria should always be given priority over social and governance criteria.”

Even in a year of economic and geopolitical challenges, global asset managers believe demand for ESG investing will accelerate and expand further into more asset classes. This raises a number of questions: Will there be enough data to support rising demand for ESG-oriented indexes and tools? Will a global consensus develop on more than just the “E” in ESG? That is, will sufficient insights be developed on social and governance criteria? These are issues we will be sure to monitor in our discussions with global asset managers in the coming years.

This is the sixth installment of a series from the Index Industry Association (IIA). The IIA is celebrating its 10th anniversary in 2022. For more information, visit the IIA website at www.indexindustry.org.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

You might also be interested in

Private Markets Are Opening Up. Now They Need to Become More Transparent.

As more investors and advisors gain access to private markets, they need reliable ways to compare opportunities,…

Voices of the IIA: A Conversation with Amelia Furr

In this episode of Voices of the IIA , Morningstar Indexes President Amelia Furr joins Index Industry…

New IIA White Paper Highlights Growing Demand for Transparency, Benchmarks and Governance Across Private Assets

New IIA White Paper Highlights Growing Demand for Transparency, Benchmarks and Governance Across Private Assets As capital…